“The downfall of SVB has left investors and depositors scrambling, as the domino effect threatens the stability of the global financial system.”

Introduction

The Silicon Valley Bank (SVB) is one of the leading U.S. banks in the fintech space, and its collapse has created an aftershock effect throughout the global financial system. Investors and depositors have uncertainties about the situation as the Federal Deposit Insurance Corporation (FDIC) intervenes to take control of the bank in question. In this article, we will analyze the international impact of SVB’s downfall on depositors, the financial markets, cryptocurrencies, and other banks.

Why Does It Matter?

As Emil Åkesson, Chairman and President of CLC & Partners, stated in his article on nasdaq.com, “If things are bad in the U.S., things are bad all over.” If the SVB issue is not addressed properly, it can lead to greater global problems with a domino effect.

Silicon Valley Bank is distinguished as being a strong stakeholder that serves tech startups, life science and healthcare companies, private equity firms, and venture capital funds. SVB stands out holding the 16th position amongst the largest banks in the U.S. with 4,100+ banks operating all over the country. Its collapse has sent shockwaves throughout the global markets and also raised concerns about the future of fintech, technology startups, and innovation in the U.S. economy.

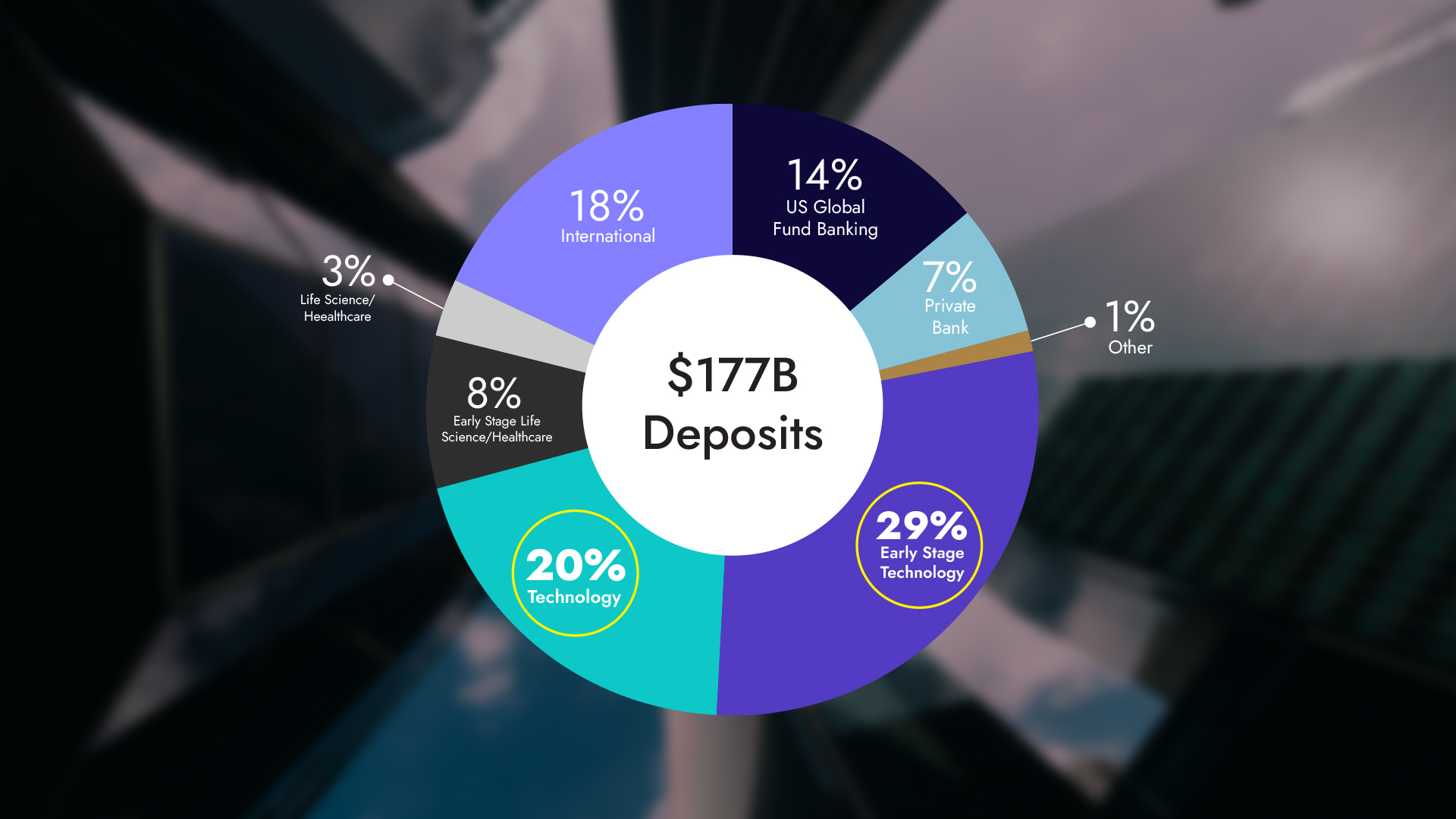

Before its breakdown, SVB’s holdings and assets were valued around at $210 billion, with $175 billion in deposits. Although this may seem like a small fraction of the total U.S. bank deposits of $18 trillion, it’s important to note that nearly $6 trillion of those deposits are held in small banks. In addition, SVB falls into the category of large banks, with its size and efficacy in the fintech industry being significant factors. In fact, this is the largest bank failure in the U.S. since 2008 Washington Mutual Bank failure.

The impact of SVB’s breakdown extends beyond its immediate clients. As the primary financial supporter of technology startups and venture capital funds, SVB’s failure could hinder the growth and development of future tech giants like Apple, Google, and Tesla in their early days. These startups rely on funding from various sources, especially venture capital firms. SVB plays a critical and central role in this ecosystem by providing commercial banking services to these companies and funds, fueling the technological innovation that has made the U.S. a global powerhouse. Therefore, it is essential for the U.S. to serve a safe and sound banking system to secure its position in the technology race.

Approximately, 29% of SVB’s deposits belong to technology startups and companies, potentially putting the next generation of industry-disrupting ideas at risk. The collapse of SVB is not only a financial crisis but also a potential innovation catastrophe. As these tech startups and venture capital funds search for new banking partners and possible financing opportunities, the U.S. must address the reverberations of SVB’s breakdown to preserve its status as a leader in innovation and prevent a possible slowdown in the growth of its tech sector.

How Did SVB Get Here?

We can trace the roots of SVB’s collapse back to 2022, when the U.S. raised interest rates to combat inflation, successfully lowering the inflation from 9% to 6% and aiming to further reduce it to 4%. As interest rates increased, the availability of capital diminished. SVB and similar banks had been providing cash flow to startups, with investors channeling their money into venture capital funds to support these projects. The startups would then use the funds to grow and eventually repay their debts. If these startups succeeded, the venture capital funds would generate substantial returns for their investors, despite the high risk.

However, the interest rates started to rise in 2022, and investors shifted their attention to low-risk deposits and bonds with higher yields which led to difficulties for venture capital funds in raising capital. Consequently, startups encountered challenges in securing funds and even struggled to pay their employees’ salaries. With the decrease in fundraising traffic, startups had to dip into their SVB bank accounts to cover these expenses, causing SVB’s total deposits to shrink. Simultaneously, SVB’s investments and shares in these sectors suffered as the startups and tech companies could no longer grow.

SVB held the top position in the Q4 of 2022 with 55.4% of their total funds invested. The bank’s deposit funding predominantly consisted of early tech startups and tech companies, providing them with fundraising by acquiring shares and receiving interest payments in return. Both investors and companies held their money in SVB, which the bank then used to make risky investments in more startups. However, with an investment-to-holding ratio of over 55%, SVB’s exposure was a very high and unorthodox one.

Ultimately, SVB failed to accurately assess the risks associated with their investments in these startups given rising interest rates. While it may not be fair to label this approach as inherently flawed, the uncontrolled inflation rate necessitated an increase in the interest rates, which proved to be the tipping point. In the end, SVB found itself unable to repay the $175 billion in deposits. The following day, SVB experienced a bank run and panicked customers withdrew $42 billion from SVB. To cover the shortfall, the bank attempted to sell its shares in tech startups and companies which led to a significant drop in their value and intensified the crisis.

The Bond Backlash

A sudden surge in interest rates can create a chain of events that sends shockwaves throughout the financial landscape, shaking the very foundation of previously issued bonds. The allure of new bonds, offering higher returns in the wake of rising interest rates, leads investors to flee for safer havens with high returns, outshining the older bonds with lower yields. As a result, bondholders seeking to sell their older bonds must reduce the prices to compete with the more appealing new bonds and this eventually leads to a capital loss.

Banks generally tend to have big holdings of government bonds that they can easily liquidate in times of crisis. Unfortunately, SVB had made considerable investments in long-term bonds when the interest rates were much lower than they are now. When the U.S. aggressively raised interest rates by 4.5%, the market value of SVB’s older long-term bonds experienced a sharp decline. This situation resulted in a $1.8 billion loss in the market value of their bond investment for SVB. These consecutive events dealt a double blow to the bank, ultimately contributing to SVB’s collapse.

The FDIC and Depositor Insurance

In the United States, the deposits are insured up to at least $250,000 per depositor in the FDIC-insured banks providing a safety net for depositors in case of bank failures. However, this limit has become a discussion topic with the SVB case.

SVB’s Q4 2022 data revealed that only 2.7% of its account holders had deposits below $250,000, which means 97.3% of the depositors had uninsured amounts exceeding the FDIC limit. These uninsured deposits are at risk of being lost, amounting to over $150 billion.

- The Existentialists: People made their own decisions and therefore should face the consequences of their own choices.

- The Concerned: If the FDIC and the government don’t intervene, it could lead to a much bigger financial crisis, affecting everyone on a global scale.

SVB, Stocks, and Commodities

SVB’s collapse has had a significant impact on global markets, with financial stocks losing $465 billion in market value in just two days. Gold prices have rallied by up to 10% as investors were seeking a safe haven. With this incident, the U.S. might have failed to fight inflation, at least for a while.

SVB and Cryptocurrencies

The collapse of SVB have had a notable impact on cryptocurrencies, particularly Bitcoin and Ethereum being the safe haven of the crypto market, which have surged in value following the bank’s downfall. Around $100 billion has moved to the crypto market in the following week, making Bitcoin, Ethereum, and altcoins such as Solana and Cardano reach new heights. Investors have been driven away from traditional banking towards the decentralised, leading to Bitcoin reaching a nine-month high.

However, every silver lining has a cloud. USDC, a stablecoin pegged to the U.S. dollar and managed by Circle, serves as a reliable medium of exchange without the volatility of other cryptocurrencies. Circle maintains a one-to-one reserve, holding one dollar for each USDC issued. Of the $40 billion raised from users, Circle invested $32 billion in short-term U.S. government bonds, securing 77% of the funds. The remaining 23%, or $3.3 billion, was held in cash, leaving 8% of USDC’s backing at risk. As a result, the theoretical value of 1 USDC should have dropped to $0.92 at the moment, casting a shadow over the stability of stablecoins.

Following the SVB news, Circle’s delayed response caused USDC’s value to plummet to the $0.8 range. Eventually, Circle announced that they had anticipated the situation and requested SVB to return the funds. U.S. regulators intervened, and USDC’s value returned to normal levels.

Circle has also stated that they are also committed to compensating for any losses if they cannot recover the funds from SVB. While this may not be a significant challenge for Circle, as they earn approximately $1.6 billion in interest annually from their bond investments, the primary issue was their delayed statement. However, Circle should have made this statement earlier to prevent panic selling and financial loss for USDC holders.

Why Blockchain Technology Shines?

While all of these were happening, some of the C-levels of the SVB were selling their shares. Gregory W. Becker, CEO of SVB, sold 11% of his shares on 27th February. Some of them started to sell their shares even more than a month ago starting at the beginning of February. Even though it was publicly available, nobody can blame individuals in a situation where the government itself couldn’t foresee and prevent this from happening. On a legal level, there seems no problem with this, but in terms of ethics, it does not look good, and Greg Becker may have a hard time finding support.

The SVB collapse highlights the advantages of blockchain technology, which offers transparency and traceability. In a centralized banking system, individuals must trust the bank, and tracing transactions can be difficult even for governments. With blockchain, all transactions are transparent and immutable, and warning systems such as Blocknative can be put in place for significant withdrawals like the SVB scandal. If this had occurred on a blockchain-based platform, investors could have been warned earlier when the bank’s C-level executives sold their shares. Unfortunately, the fintech industry has failed in educating the public about these warning system benefits. This highlights the need for improved communication and transparency in the financial industry and as CLC & Partners, we are committed to informing our audience.

The 3S Trio: Silvergate, SVB, and Signature Bank

Silvergate Capital, SVB, and Signature Bank, all facing financial issues, have caused turmoil in the crypto-friendly banking space. The closures of these banks, coupled with regulatory and legal investigations, have made it difficult for crypto companies to rely on traditional banking partners.

What’s Next for SVB and Its Depositors?

A consortium of private equity firms led by The Bank of London has submitted formal proposals to His Majesty’s Treasury to acquire SVB, but it remains uncertain whether the U.S. government will allow such a move due to potential privacy concerns.

U.S. Treasury Secretary Janet Yellen has announced that there will be no bailout for SVB. However, Yellen and the FDIC declared that additional funding will be made available to ensure all deposits will be paid in full regardless of the amount. The Fed also plans to provide funding to eligible depository institutions to support depositor needs. It should be noted that this issue should be solved very carefully to avoid providing freedom and relief to the other banks in the U.S. in terms of taking relentless risks with such a remedy.

Conclusion

All in all, the dramatic downfall of Silicon Valley Bank has left far-reaching consequences, affecting investors, depositors, and the global financial system. While the FDIC and the government are stepping in to prevent a total meltdown, it’s essential to monitor the situation closely and learn from this crisis to better prepare for future financial disruptions. As our chairman and president Emil Åkesson says, “history repeats itself, again,” and it will sure do again. A detailed case study like this article will definitely help us to extract valuable lessons to safeguard against future economic disruptions.

The financial world needs a leap forward, and we at CLC & Partners are eager to provide our community with our team’s valuable insights and extensive experiences to help you stay ahead of the curve. Follow CLC Blog to stay tuned and with truth!